Introduction

A Written Information Security Plan (WISP) is not optional for financial firms in 2026.

It is a required cybersecurity control under regulations like the FTC Safeguards Rule—and one of the first things auditors, regulators, and cyber insurance providers will ask for.

If your firm does not have a documented, enforceable WISP, you don’t just have a gap…

👉 You have a compliance risk and a liability issue

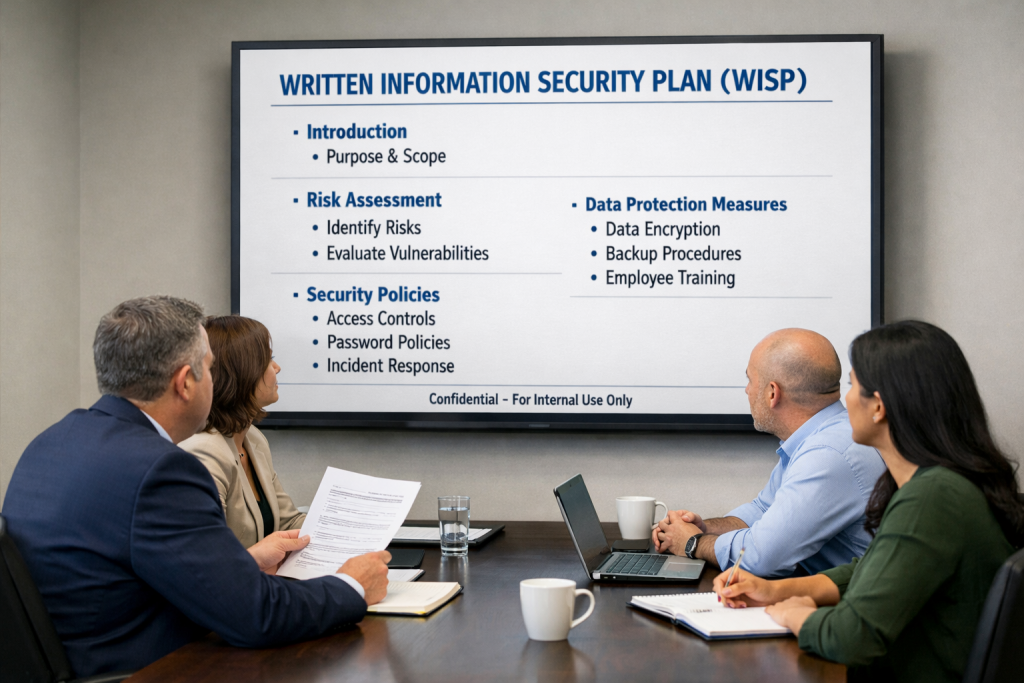

What Is a Written Information Security Plan (WISP)?

A WISP is a formal, documented plan that outlines how your firm:

- Protects sensitive data

- Manages cybersecurity risks

- Enforces security policies

- Responds to incidents

Think of it as:

The blueprint that proves your firm takes cybersecurity seriously—and can back it up.

What a WISP Typically Includes

A properly structured WISP should define:

- Risk assessment processes

- Access control policies

- Data protection measures

- Employee training requirements

- Vendor management procedures

- Incident response planning

- Ongoing monitoring and review

It’s not just a document—it’s a framework for how your firm operates securely.

Why Financial Firms Need a WISP

Financial firms handle highly sensitive data:

- Client financial records

- Personally identifiable information (PII)

- Account access and transaction data

Because of this, regulators require firms to:

👉 Identify risks

👉 Implement safeguards

👉 Document and enforce those safeguards

Regulatory Expectations

Under the FTC Safeguards Rule and similar standards:

- A WISP is required—not recommended

- Firms must designate responsible individuals

- Security controls must be documented and maintained

Cyber Insurance Expectations

Insurance providers increasingly require:

- Proof of policies

- Documentation of controls

- Evidence of enforcement

No WISP often means:

- Higher premiums

- Limited coverage

- Or denied claims

What Most Financial Firms Get Wrong

Most firms fall into one of these categories:

❌ They Don’t Have a WISP at All

They assume IT tools cover them

❌ They Have a Template Sitting on a Shelf

Generic, outdated, and not tied to their environment

❌ It’s Not Enforced

Policies exist—but no one follows or monitors them

❌ No Ownership

No assigned responsibility for maintaining the plan

A WISP that isn’t enforced is just paperwork—and it won’t protect you in an audit or a breach.

What “Good” Looks Like in 2026

A properly implemented WISP is:

✅ Customized to Your Firm

Reflects your actual systems, risks, and workflows

✅ Actively Maintained

Updated regularly as your environment changes

✅ Enforced Across the Organization

Policies are applied consistently—not optionally

✅ Assigned Ownership

A designated individual is responsible for oversight

✅ Backed by Evidence

You can show:

- Logs

- Reports

- Training records

- Policy enforcement

In other words—you don’t just have a plan. You can prove it’s working.

How to Build or Fix Your WISP

If your firm doesn’t have a WISP—or isn’t confident in it—start here:

- Conduct a Risk Assessment

Identify where your biggest exposures are - Document Your Policies

Access control, data handling, incident response, etc. - Align Controls to Real Systems

Tie policies to actual tools and processes - Assign Ownership

Someone must be accountable - Implement Monitoring & Review

Ensure policies are enforced and updated regularly

Who This Applies To

This applies directly to:

- Financial advisors

- CPA firms

- Wealth management firms

- Tax and bookkeeping firms

If your firm handles sensitive financial data, a WISP is required.

Download the Full Guide

A WISP is just one of the 12 cybersecurity controls your firm should have in place.

👉 Download: “12 Cybersecurity Controls Every Financial Firm Must Have in 2026”

Inside, you’ll get:

- A full checklist

- Common gaps we see in financial firms

- A simple way to assess your current risk

🔚 Closing Thought

Cybersecurity is no longer about what you have installed.

It’s about what you can prove.

And your WISP is where that proof starts.